According to Fidelity Investment’s 2023 Small Business Retirement Index, only 34% of small businesses are currently offering retirement savings to employees and 21% don’t know how to start the process of offering a retirement plan, or which retirement plan vehicle works best for them.

Small business owners are faced with many challenges as they grow their business, therefore, being tasked with knowing the differences between a SEP IRA, SIMPLE IRA, and 401(k) can be intimidating.

To offer some color around a few common plan types let’s dive into the differences between a SEP IRA, SIMPLE IRA, and 401(k)!

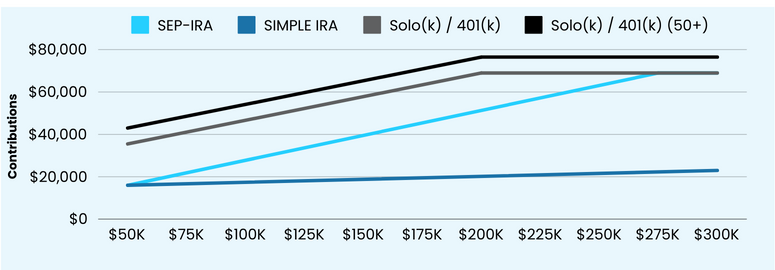

The graph below illustrates maximum contributions to the three retirement plan options by income level. As you can see, at every income level, the Solo 401(k) and 401(k) Profit Sharing Plans allow plan participants to contribute more towards retirement than the two other retirement plans.

As you can see, Solo(k)s and traditional 401(k)s not only offer higher contribution limits, but also offer more flexibility in design to manage business costs, taxes, and enable penalty-free access to funds via a loan if an emergency arises. Contact us today to discuss which plan design may best suit the needs of your business owner clients!