By 2025, most startup retirement plans will be required to automatically enroll new employees into their plan, unless they opt out, at an initial 3% employee deferral rate with auto escalation. – Sound familiar?

The SECURE 2.0 automatic enrollment mandate states an initial automatic enrollment at a 3% employee deferral rate with 1% automatic escalation up to 10% but no more than 15%. In contrast, a Qualified Automatic Contribution Arrangement (QACA) Safe Harbor has initial automatic enrollment at a 3% employee deferral rate with 1% automatic escalation of up to 6%.

Meaning, with a slight adjustment to the auto escalation requirement, a QACA operates as a Safe Harbor and satisfies the new mandate.

Benefits from implementing a Safe Harbor plan include, but not limited to, passing ADP/ACP testing, avoiding corrective distributions and/or initially satisfying Top Heavy minimums.

But wait! There’s more… let’s explore why a QACA Safe Harbor may be considered the new norm over a Traditional Safe Harbor approach.

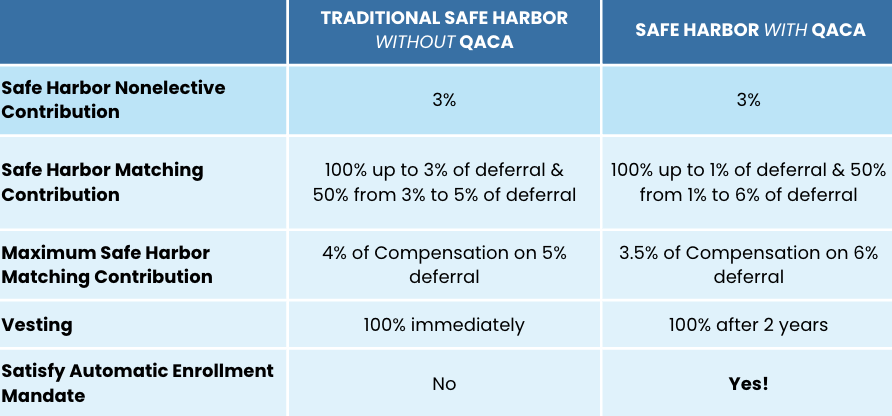

Below is a chart used to compare the differences between Traditional Safe Harbor and Safe Harbor with QACA.

In summary, leveraging a Traditional Safe Harbor strategy to maximize benefits for HCEs has been standard practice; however, since the passage of the SECURE Act 2.0, one could argue a new norm is upon us.

Not only do you get the benefits of a lower match obligation and a stretched vesting schedule; adopting a QACA Safe Harbor plan design can also meet the auto enrollment mandate for newly established retirement plans.

At My Benefits we strive to be a driving force for innovation within our industry by leveraging our expertise and navigating new regulations to tailored, proactive and accurate retirement plan solutions.

Your retirement plan questions answered, in plain English, by an expert. Use the form below to ask our retirement plan experts your question.